Firms Look for Wider Nets to Oversee Rep-As-Portfolio-Manager Growth

Just as Chief Brody kept vigilant watch over his beach for a predatory shark, wealth management executives must also maintain thorough oversight of advisors who make use of rep-as-portfolio-manager (RPM) platforms. The business threats are real, with rogue advisors lurking below the waves, feeding off home office lax supervision.

Broker-dealers should outfit their oversight and monitoring processes with solutions that offer scale and flexibility as the number of advisors, clients and transactions on these platforms grow.

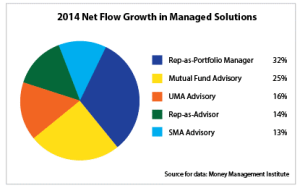

RPM platforms are gaining assets because they allow advisors to offer personalized and responsive investment strategies and provide higher revenue streams from portfolio management fees. Net asset flows into RPM programs accelerated in 2014, rising 32 percent according to the Money Management Institute.

responsive investment strategies and provide higher revenue streams from portfolio management fees. Net asset flows into RPM programs accelerated in 2014, rising 32 percent according to the Money Management Institute.

The trend of steady growth in RPM platforms has been building for several years. Independent advisors were among the first champions of these platforms, but after a wave of early adoption, RPM growth has slowed in the independent channel according to research by Securities Service Network (SSN). However, wire house and national firm reps have fueled more of the recent rise of these programs as they seek to compete with the “hands-on” personalized services offered by independent RIAs.

Market volatility may push more advisors in the RPM direction and bring more clients onto these platforms as they seek safe havens for their formerly self-directed portfolios. SSN estimated strong AUM growth for wire house and national firm advisors who utilize RPM programs.

For an advisor, RPM programs offer a higher degree of discretion to manage client assets and respond to shifts in market trends or investor sentiment. RPM platforms allow advisors to build and manage portfolios to meet specific objectives, such as current income, or to invest in a manner that follows a client’s ethical principles, such as religious guidelines or social responsibility.

But with greater discretion comes a higher potential for abuse. Firms need to establish and maintain sufficient controls and oversight to track RPM trading activity, monitor asset allocations, and detect performance outliers.

A number of fintech vendors have announced software solutions that make oversight of RPM platforms more efficient and cost-effective. Many programs allow firms to establish “guardrails” and pre-define the universe of securities available to minimize potential conflicts of interest and keep themselves and their advisors compliant with fiduciary standards.

In addition, pre- and post-trade compliance tools help ensure sufficient supervisory protocols are in place across the board. Trade monitoring is especially important when YTD F markets become turbulent and volume spikes occur in riskier investments and securities.

turbulent and volume spikes occur in riskier investments and securities.

Regulatory organizations such as FINRA are scrutinizing the results advisors achieve in RPM programs to ensure they match their stated objectives. They are especially focusing on “aggressive growth” portfolios that have a higher potential for abuse.

Advisory firms are seeking automated tools that make it easier to spot performance outliers and review underlying holdings and transactions in RPM portfolios. This is to ensure that proper monitoring is in place so that they are able to identify unscrupulous activity before clients are harmed.

For instance, FINRA is requiring the home office of BDs to review all “aggressive growth” portfolios across all RPMs, find outliers in terms of performance outcomes, and investigate their underlying holdings, transactions, etc. for issues.

Lack of sufficient oversight can come at a significant financial cost to a firm. Earlier this year, FINRA hit LPL Financial with a $10 million fine and ordered $1.7 million in restitution payments to clients. FINRA charged the broker-dealer with “broad supervisory failures” for transactions involving a wide range of investments and products, including alternative exchange-traded funds and other complex securities.

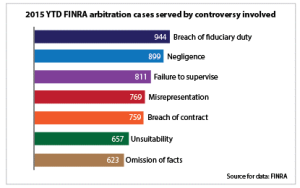

High on FINRA’s current watch list are violations that related to RPM programs. The top three charges for FINRA arbitration cases thus far in 2015 are for breach of fiduciary duty, negligence, and failure to supervise. Any compliance solution that a broker-dealer is considering for expanding their oversight of RPM platforms should cover these areas and more.

Fines aren’t the only costs firms may face when they don’t adequately supervise advisors on their RPM platforms. Negative publicity can impact a firm’s reputation when advisors go rogue and are sued by former clients. The PR damage can be exceptionally high when the clients involved are high-profile celebrities or professional athletes. Lawsuits filed by famous clients against their financial advisors often garner media attention beyond business news, landing on the sports and entertainment pages.

A robust oversight solution will be critical for broker-dealers should the Department of Labor’s proposed revision of the fiduciary rule become reality. Firms will need to pledge that they have adequate rep oversight in place, not only to stay compliant themselves but to help their advisors follow the letter of the new ruling as well.

Oversight is becoming more important as RPM programs expand to take on more clients, more assets, and more transactions. Wealth management firms are going to need bigger and better tools with more powerful reporting that can go deeper and wider in monitoring advisors as their RPM platforms grow.

Learn how a single tool can help your firm calculate the analytics needed, automate the identification of an outlier, give risk, and asset allocation perspective within an agreed-upon SLA, and provide a workflow solution to track the mitigation steps and documentation to support a regulator’s audits. To learn more, contact First Rate today to learn how to manage oversight of your Rep-as-PM program.

Craig Iskowitz is CEO and founder of Ezra Group, LLC, located in East Brunswick, NJ. Ezra Group is a management consulting firm providing advice to the financial services industry on business and technology strategy, software development, and marketing.